We are a fintech that's making money easier.

Business overview

| Location | Essex, United Kingdom |

|---|---|

| Social media | |

| Website | www.zazuafrica.com |

| Sectors | Finance & Payments Digital B2C |

| Company number | 09829173 |

| Incorporation date | 19 Oct 2015 |

Investment summary

Business highlights

- Now a Mastercard Principal Member

- Launched Virtual Debit Cards in July 2020

- Launching Contactless Debit Cards in October 2020

- Investment conditional upon Future Fund funding - see Key Info

Key features

Learn more about convertible loan campaigns.

Idea

Introduction

We want to make money simpler for everyone in Africa, starting in Zambia. To do that, we have developed a debit card connected to an app. The app gives people control over how and where their money goes, in addition to expense categorisation and real-time peer to peer payments. Meeting the moment, we've recently released virtual debit cards, giving people an extra level of safety for e-commerce transactions.

We recently became a Mastercard Principal Member. In the short term, this has enabled us to launch faster and without depending on any commercial banks. In the long term, this opens up a number of interesting opportunities.

Our vision is to develop the financial infrastructure for Africa, chipping away at the dependency on foreign systems that are expensive and slow to effect payments. We've recently announced Union54 - an attempt to standardise the African payments landscape, expected to launch in Q1 2021 in a number of African markets.

Substantial accomplishments to date

December 2017: Closed a round on Seedrs to build the platform.

July 2018: CEO, Perseus Mlambo Named on Forbes 30 Under 30.

August 2018: Licensed by Bank of Zambia as a Payments System Business.

March 2019: App Beta begins.

June 2019: 1,000 users on app.

June 2019: Won a contract to payout $650,000.

August 2019: Received a $1.4 million grant to grow the business.

April 2020: Mastercard Principal Membership obtained.

July 2020: Zazu virtual debit cards launched.

October 2020: Zazu physical cards to launch.

Monetisation strategy

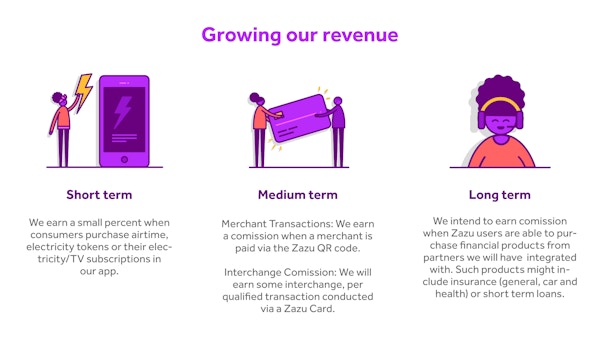

Short term:

1. We earn a small percent when consumers purchase airtime, electricity tokens or their electricity/TV subscriptions in our app.

2. We also earn a negligible amount of interest on balances held in our bank accounts.

Medium term:

1. Merchant Transactions: We earn a commission when a merchant is paid via the Zazu QR code.

2. Interchange Commission: We will earn some interchange, per qualified transaction conducted via a Zazu card.

Long term:

1. We intend to integrate to other financial service providers and enable our users to purchase products from them. We think we might activate insurance and lending products in the medium term, earning a commission per qualified transaction.

2. We will earn money by charging people to use our product. Fees might be bundled into a monthly fee, or they might be pay per product e.g. a virtual card is $1 to create, or a debit card is $2 to order etc.

Use of proceeds

We now have the regulatory approvals, and a beta product being used by customers and are developing our feedback loops. We have been very capital efficient to get to this point and intend to retain that culture as we start finalising potential pathways to scale. This bridge round will be used to achieve the following milestones:

1. Integrating into an identity solutions provider to enable us to onboard customers outside of Zambia.

2. Setting up multi currency services in the Zazu app and release paid-for products.

3. Invest in paid marketing as we ramp up user growth.

4. Continuous product development and market feasibility studies.

Key Information

Seedrs is supporting companies who are intending to apply to the Government backed Future Fund. You can read more about the Future Fund here: https://www.seedrs.com/learn/blog/the-future-fu....

In order for a company to be eligible to seek matched funding from the Future Fund, this investment round must be on the convertible loan terms that have been prescribed by the Future Fund for this purpose. These terms differ to our normal ‘advanced subscription agreements’.

Given this product differs from most campaigns on Seedrs, we urge all investors, including regular Seedrs investors, to read the information below and ensure you understand the terms in full before making your investment.

Key terms

You will see a term sheet attached to this Campaign in the Documents section which sets out the key terms of the convertible loan and you can see the full document prescribed by the Future Fund here: https://www.british-business-bank.co.uk/ourpart....

A summary of the key terms is set out below, but should be read in conjunction with the term sheet:

• Discount: 20%

• Interest: 8% per annum, non-compounding. On conversion events, the company can choose to repay the interest or convert it to equity (generally without the discount). See the Term Sheet for more details.

• Redemption Premium: An amount equal to 100% of the principal loan amount

• Qualifying Equity Financing. The convertible loan will automatically convert on an equity financing raising at least the total loan amount, at the lowest share price of equity financing less the Discount.

• Maturity Date: 36 months from signing convertible loan agreement.

o The default position is on the maturity date is that the loan will convert to equity unless the investor majority elect to redeem.

- If redeemed, the company will repay the principal together with the Redemption Premium.

- If converted, the conversion price will be at the most recent funding round share price less the Discount, provided that funding round happened after 20 April 2020 and was at least a quarter of the size of the convertible loan investment. If no such funding round has occurred, conversion will be at the share price of the last funding round prior to 20 April 2020 (no Discount).

• Other events of default or conversion: There are various other scenarios in which the convertible loan may convert or be repaid and investors should reference the term sheet:

o Non Qualifying Funding Round: The convertible loan can convert on an equity financing round which does not meet the size criteria of a ‘Qualifying Equity Financing”, at the election of the majority of investors under the loan. Please see the term sheet for how this conversion is priced.

o Exit: The convertible loan will automatically convert or be redeemed on an Exit, whichever would give investors the higher cash return. Please see the term sheet for how conversion is priced and payments on redemption in this scenario.

o Events of Default: The convertible loan is to be repaid on the events of default, such as liquidation or winding up. See the term sheet for more details.

Government matched funding

The company intends to apply to the Future Fund for matched funding on the total eligible amount invested in this funding round. The Future Fund will “match” the funding raised via Seedrs or other eligible sources, subject to a minimum investment of £125,000 and a maximum investment of £5m. The Future Fund is to be allocated on a ‘first come, first served basis’, so there is no guarantee that a company will receive the Future Fund matched funding.

This campaign is conditional upon receiving matched funding from the Future Fund. Seedrs will not complete the investment and transfer the funds raised until we have confirmation that the Future Fund matched funding application has been approved and that the Future Fund is ready to make the investment. If the application is denied, the campaign will be cancelled and funds will be returned to investors.

Because this campaign is conditional upon the matched funding, you will see that we have reflected the Future Fund investment as part of the round. It is distinguished in pink in the progress bar of the campaign. This is to give investors an indication of the potential total size of the funding round (and potential dilution on conversion), but to also distinguish it from regular investment through the Seedrs platform.

Seedrs does not charge any fees in relation to the Future Fund matched funding, application process or for acting as lead investor with respect to applications.

Conversion to equity

The convertible loan agreement prescribed by the Future Fund is equity focused and favours conversion of the loan to equity as the default position.

Redemption is only available in certain scenarios and is often subject to the vote of majority of the investors. Where a vote of investors is required, Seedrs will vote on behalf of any investors it represents as nominee.

There is a possibility that the convertible loan will convert in some scenarios without the consent of Seedrs (if we do not make up a majority of investors). It is also Seedrs’ position that this is primarily an instrument for investing in the equity of the fundraising business and our default position would be to vote in favour of converting the loans to shares in the company, unless there is a clear or compelling reason not to.

Risks

As always, investors should be aware of and accept the risks involved in investing in early stage and growth focused businesses: https://www.seedrs.com/pages/risk-warnings

In addition to the usual risk warnings included above, investors should be aware of and accept the following with respect to convertible loans:

• The convertible loan agreement is intended as bridge funding to a future funding round, but there is no guarantee that a company will be able to secure further funding.

• The Future Fund is to be allocated on a ‘first come, first served basis’ and there is no guarantee that a company will be successful in its application to receive the Future Fund matched funding.

• There is a risk that the Company may not have sufficient funds to repay the loan on the maturity date, pay interest when it becomes due or pay the redemption premium included in the terms.

• Convertible loans are unsecured obligations and in the event of a winding up or liquidation event will rank behind secured creditors of the Company.

Secondary market

Investors will not be able to sell their interest in the convertible loans on the Seedrs Secondary Market unless and until they have converted to shares in the company (and then only subject to eligibility and the terms and conditions of the Seedrs Secondary Market).

EIS Relief - past, current and future

As noted above, the convertible loan instrument is not compatible with EIS requirements, so no EIS applications will be made with respect to investments in the convertible loan.

The government has confirmed that investing in the convertible loan will not impact EIS relief previously claimed on investments in the fundraising company:

“The government has confirmed that such previous investments will not be affected where the convertible loan converts into shares. Where the convertible loan note redeems, we have been alerted that the government intends to make changes to the rules to clarify that this is compatible with such previous investments.”

However, investing in a convertible loan could impact your ability to claim EIS relief on future investments into the same company. The government has not clarified the position on this and has said it is a matter for HM Treasury and HMRC.

Seedrs is unable to provide tax advice. Tax treatment depends on individual circumstances and is subject to change.

Open an account to get access to the team members of Zazu

Already have an account? Log in

To comply with financial regulations, we can only show full campaign details to registered users.

Open an account to get access to the Zazu campaign updates

Already have an account? Log in

To comply with financial regulations, we can only show full campaign details to registered users.

Open an account to get access to the list of investors in the Zazu campaign

Already have an account? Log in

To comply with financial regulations, we can only show full campaign details to registered users.

Open an account and verify your identity to get access to the Zazu discussion

Already have an account? Log in

To comply with financial regulations, we can only show full campaign details to registered users.

Open an account and verify your identity to get access to the Zazu pitch deck and other documents

Already have an account? Log in

To comply with financial regulations, we can only show full campaign details to registered users.