Tax And The Benefits Of Investing In Startups

Investing in startups is crucial to the future of our economy and wider society. Over the past few decades startups have transformed the way we live, and driven vast growth in GDP across the world, which governments are keen to supercharge.

Startups can be very capital intensive. In order to focus on innovation and growth, traditional business fundamentals of revenue and profitability can take a back seat, so startups need to raise money from investors who are happy to invest their cash in exchange for equity.

To encourage investment into startups, governments around the world have created tax efficient schemes to make these sorts of investments more appealing to investors within their countries. These schemes offer sizable tax breaks on initial investments, exits, and losses, encouraging investors to allocate some of their portfolio to eligible businesses.

Previously these schemes were difficult for retail investors to access, given the high ticket sizes associated with investing in startups. Platforms like Seedrs have made it possible for investors from any walk of life to access these tax breaks.

What are the potential tax benefits for UK investors in UK startups?

There are two main schemes available to UK investors investing in individual private companies:

Via these schemes, UK investors can receive up to 50% Income Tax relief on their principal investment, exemption from Capital Gains Tax on any gains from the investment, Capital Gains Tax deferral relief, Inheritance Tax relief, and Income Tax loss relief on at risk capital for failed investments. We cover each scheme in more detail below.

What is the Enterprise Investment Scheme (EIS)?

The Enterprise Investment Scheme (EIS) is a government-backed scheme that aims to help smaller companies raise finance by providing tax reliefs to investors who purchase shares in these companies. The scheme was introduced in 1994 and has since become one of the most popular tax-efficient investment schemes in the UK.

What are the benefits of EIS?

EIS provides significant tax relief for investors. The main benefits are;

- 30% Income Tax relief on EIS investment amount

- Capital Gains Tax exemption on profits made from EIS shares

- Offset losses on EIS shares against Income Tax

- Capital Gains Tax deferral

- Inheritance Tax exemption on EIS shares

EIS Income Tax relief

An investor who invests cash for ordinary or non-cumulative fixed preference shares in an EIS qualifying company can obtain Income Tax relief of up to 30% on investments of up to £1m each year.

According to HMRC, this relief can be claimed either in the tax year the investment is made, or in the previous year. Income Tax relief is limited by the amount of tax paid by the investor – it can reduce the investor’s tax liability to nil, but no more.

EIS Capital Gains Tax relief

Once an investor has held EIS shares for at least three years, when shares are sold the gains will be Capital Gains Tax free, provided Income Tax relief has been given and has not been withdrawn.

EIS Loss relief

If a loss is made on the sale of EIS shares at any time, the loss, net of Income Tax relief, may be claimed against either current year or future capital gains, or against income of the current or previous tax year. For a 45% taxpayer, this reduces the loss as follows:

EIS eligible initial investment: £10,000

Income Tax Relief at 30%: (£3,000)

At risk capital: £7,000

Loss relief: 45% of £7k = (£3,150)

Net loss: £3,850

EIS Capital Gains Tax deferral

Investors with capital gains made up to three years before or one year after an EIS investment is made can claim ‘deferral relief’ against those gains based on the initial investment amount into EIS eligible businesses.

The tax will need to be paid when:

- you dispose of the investment

- the investment is cancelled, redeemed or repaid

- the company stops meeting the scheme conditions

- you become non-resident

Deferral relief is available even if Income Tax relief is not because you’re associated with a business.

EIS Inheritance Tax exemption

If an investor has held shares in an EIS eligible business for at least two years and certain conditions are met at the time of transfer, inheritance tax business property relief of 100% can be applied. This reduces the inheritance tax liability on the transfer to 0.

There is no limit on the amount a shareholder can invest in EIS companies for inheritance tax relief purposes.

What are the rules for EIS?

To benefit from these tax breaks, investors must meet certain eligibility criteria;

- Be a UK taxpayer and be over 18

- Hold no more than 30% of the company’s shares

- Not be employed by the company unless they’re a director

- Must not receive any benefits from the company other than their return on investment.

Any qualifying individual can invest up to £1m under the scheme each tax year. This increases to £2m if at least £1m is invested in ‘Knowledge Intensive Companies’. Income Tax relief can be claimed on EIS shares in the tax year that the shares were purchased, or the tax year prior. To benefit from the Capital Gains Tax exemption, shares must be held for 3 years from the date of issuance.

How can investors benefit from EIS and access EIS investments?

Investors can access EIS business through a range of platforms and investment providers. Some investors choose to invest directly in individual companies, while others prefer to invest through EIS funds or trusts.

If you are an investor looking to benefit from some of these tax relief schemes, you can explore EIS eligible businesses that are currently raising capital on Seedrs now.

What is the Seed Enterprise Investment Scheme (SEIS)?

The Seed Enterprise Investment Scheme (SEIS) is another government-backed scheme, similar to EIS, that aims to help even earlier stage companies raise their first financing by providing enhanced tax reliefs to investors who purchase shares in these companies. The scheme was introduced in 2012 to complement EIS and drive investment into even earlier stage businesses.

What are the benefits of SEIS?

SEIS provides even more significant tax relief for investors. The main benefits are;

- 50% Income Tax relief on SEIS investment amount

- Capital Gains Tax exemption on profits made from SEIS shares

- Capital Gains Tax reinvestment relief

- Offset losses on SEIS shares against Income Tax

- Inheritance Tax exemption on SEIS shares

SEIS Income Tax relief

An investor who invests cash for ordinary or non-cumulative fixed preference shares in an SEIS qualifying company can obtain Income Tax relief of up to 50% on investments of up to £200k each year.

This relief can be claimed either in the tax year the investment is made, or in the previous year. Income Tax relief is limited by the amount of tax paid by the investor – it can reduce the investor’s tax liability to nil, but no more.

SEIS Capital Gains Tax relief

Once an investor has held SEIS shares for at least three years, when shares are sold the gains will be Capital Gains Tax free, provided Income Tax relief has been given and has not been withdrawn.

SEIS Capital Gains Tax reinvestment relief

When an investor sells any asset and uses all or part of the gain to invest in shares that qualify for SEIS, they will not have to pay Capital Gains Tax, as long as they have sought Income Tax relief on the same investment.

Investors can get Capital Gains Tax relief on 50% of the investment, up to £200,000. So the maximum amount an investor can get is £100,000.

You do not have to sell an asset before you invest. However if you do, the asset must be sold in the same tax year that you claim Income Tax relief on the investment.

SEIS Loss relief

If a loss is made on the sale of SEIS shares at any time, the loss, net of Income Tax relief, may be claimed against either current year or future capital gains, or against income of the current or previous tax year. For a 45% taxpayer, this reduces the loss as follows:

- SEIS investment: £10,000

- Income Tax Relief at 50%: (£5,000)

- At risk capital: £5,000

- Loss relief: 45% of £5k = (£2,250)

- Net loss: £2,750

SEIS Inheritance Tax exemption

If an investor has held shares in an SEIS eligible business for at least two years and certain conditions are met at the time of transfer, inheritance tax business property relief of 100% can be applied. This reduces the inheritance tax liability on the transfer to 0.

What are the rules for SEIS?

To benefit from these tax breaks, investors must meet certain eligibility criteria;

- Be a UK taxpayer and be over 18

- Hold no more than 30% of the company’s shares

- Not be employed by the company unless they’re a director

- Must not receive any benefits from the company other than their return on investment.

Any qualifying individual can invest up to £200k under the scheme each tax year. Income Tax relief can be claimed on SEIS shares in the tax year that the shares were purchased, or the tax year prior. To benefit from the Capital Gains Tax exemption, shares must be held for 3 years from the date of issuance.

How can investors benefit from SEIS and access SEIS investments?

Investors can access SEIS business through a few platforms and investment providers. Some investors choose to invest directly in individual companies, while others prefer to invest through SEIS funds or trusts.

If you are an investor looking to benefit from some of these tax relief schemes, you can explore SEIS eligible businesses that are currently raising capital on Seedrs now.

What other options are available for tax efficient investing into startups in the UK?

Venture Capital Trusts (VCTs)

What is a Venture Capital Trust?

A VCT is a publicly listed company that pools together funds from investors to invest in VCT-qualified companies. When an investor invests in a VCT, their funds are invested into multiple businesses with one investment.

VCTs largely invest in small, entrepreneurial businesses, based in the UK. The companies can be privately owned or listed on AIM, the Alternative Investment Market of the London Stock Exchange.

To qualify for VCT investment, a company must carry out a ‘qualifying trade’. Most trades are eligible, and exclusions are made when HMRC believes the industry does not require additional support to drive investment, e.g. financial activities, farming, energy generation.

Other criteria for qualification are: being relatively small, with fewer than 250 employees and less than £15m in gross assets, and being relatively young, no older than 7 years since inception.

What tax benefits are available for investing in VCTs?

VCT investors benefit from 30% Income Tax relief on their initial investment, and Capital Gains Tax exemption on dividends paid by the VCT. Investors can invest up to £200k into VCTs with tax benefits. Any funds invested above this amount will not be eligible for tax relief.

How do investors claim S/EIS tax relief?

Whether you file your own tax return or pay tax via PAYE, you can claim tax relief relatively easily.

What’s the process for claiming S/EIS tax relief?

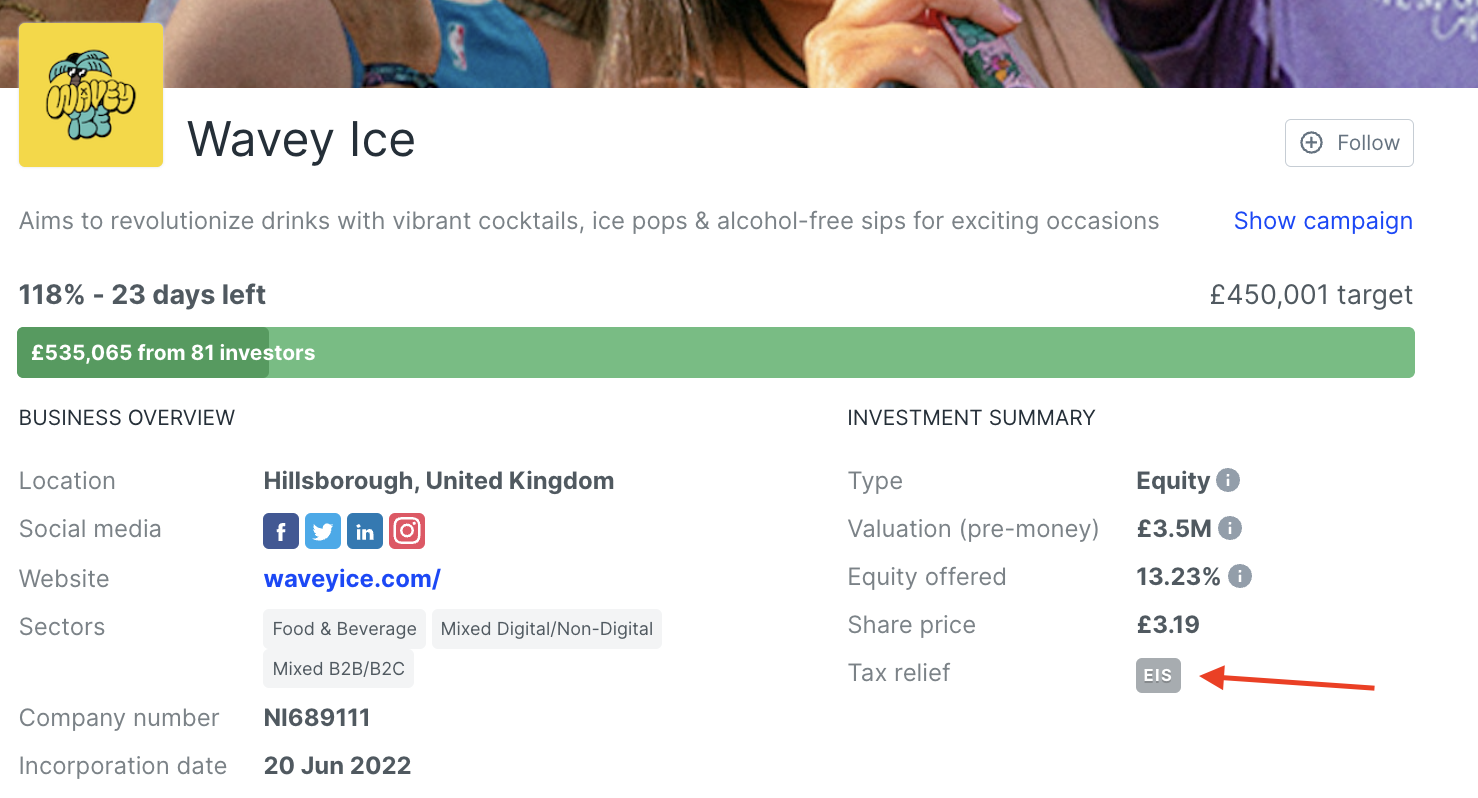

- 1. Check the company you’re investing in is tax relief eligible: this will be visible on the ‘Campaign Page’ under ‘Tax relief’

- 2. Invest in the business. Buy ordinary shares, in exchange for cash, that make up no more than 30% of the business

- 3. Wait to receive your S/EIS3 form. Once EIS relief is approved by HMRC, which will take 3-6 months, personalised EIS3 certificates will be issued to all investors. These can be found in the ‘Tax Documents’ page in your Seedrs portfolio.

- 4. Claim tax relief from HMRC. Once you’ve received your relevant forms, you can claim tax relief from HMRC. This can be done relatively easily as part of your tax return if you submit a self assessment, or the forms can be submitted to HMRC individually if you pay tax via PAYE. We will outline the process for both below:

How to claim S/EIS tax relief via a Self-Assessment tax return

You can find your S/EIS3 certificates in your portfolio page. To make it easier for investors to claim, we automatically create personalised tax statements for all of your eligible investments, which can be downloaded from the ‘Tax statements’ section of ‘Tax documents’ in your Seedrs portfolio.

- Download your Seedrs Tax statement from your Seedrs portfolio

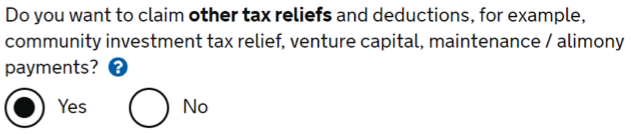

- Login to HMRC to file your self-assessment tax return. If this is your first self-assessment you’ll need to register for an account. When prompted with the question on other tax reliefs in section 3, “Tailor your return”, ‘Do you want to claim other tax reliefs and deductions…’, check ‘Yes’.

- In the section “Other tax relief and deductions (Page 2)” of section 4, “Fill in your return”, type in the total amount of all your S/EIS subscriptions on which you wish to claim tax relief and provide details of each of your S/EIS investments. The total amount can be found on the first page of your Seedrs tax statement.

If you’re claiming relief on multiple tax years, you’ll have to add up the total amount invested across all of your downloaded statements.

Be aware when submitting a statement for the current year, you can only claim relief on businesses with a UNIQUE INVESTMENT REFERENCE (UIR) – this is created when certificates are issued by HMRC.

Back to the submission: within the blank “Additional information” part at the end of section 4, you should write the Unique Investment Reference (UIR), the name of the companies invested in, the amount of the subscription and the date of issue of the shares. If you have lots of eligible investments, as many Seedrs investors do, you can attach your Seedrs Tax statement PDF(s) to your self-assessment.

- You will be shown the calculation of the tax relief for which you are eligible. Check that this is correct and click ‘Next’ to proceed.

- Your self-assessment calculation should adjust at this point. If you have already paid tax for the year in which you are claiming, you will be able to see here that you have overpaid and will be able to schedule a repayment.

How to claim S/EIS tax relief if you pay tax via PAYE

If you pay Income Tax via PAYE and want to claim EIS relief, the simplest way is to fill out pages 3 and 4 of your EIS3 certificates and submit them to your HMRC tax office. Fill out the details of your shareholding for each individual business, ensuring you tick “Tax Relief in PAYE coding”, and return this to your HMRC tax office, who will amend your tax code for the year.

You will then need to make the claim on your tax return if it is received from HMRC at the end of the tax year.